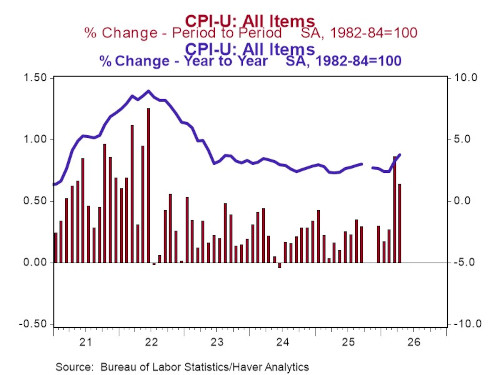

Implications: The conflict in the Middle East is still temporarily boosting measured inflation. Price increases once again came in very high but as expected in April, with the Consumer Price Index rising 0.6% following a 0.9% increase in March. The “core” CPI, which excludes food and energy, rose 0.4% on April, above the consensus expected +0.3%. The difference between headline and core inflation came from energy, with prices rising sharply (+3.8%) for the second month in a row after the outbreak of war in Iran sent global oil prices sharply higher. Energy prices accounted for 40% of the overall monthly increase, which pushed the year-ago comparison for headline inflation to a three-year high of 3.8%. While we expect the effects of higher energy costs to reverse once the conflict winds down, the timing remains uncertain, leaving the Federal Reserve with little conviction in the near term for monetary policy. In the meantime, core prices are up 2.8% from a year ago, higher than the 2.6% reading from a month ago, and still well above the Fed’s 2.0% target. Housing rents (those for actual tenants as well as the imputed rental value of owner-occupied homes) were the main driver of core inflation for the month and have been for the last few years. Recent data had hinted that rents might be finally starting to turn over, but April told a different story, with rents posting the biggest increase in more than two years (+0.5%), though much of the increase likely reflected a one-off adjustment by the BLS to correct for distortions caused by the government shutdown last fall. Other notable movers in the core group include rising prices for hotels and airline fare (both +2.8%), as well as apparel (+0.6%), and falling prices for new vehicles (-0.2%) and health insurance (-0.4%). Outgoing Fed Chair Jerome Powell at one point highlighted “Supercore” inflation – a subset category of prices that excludes food, energy, other goods, and housing rents. That measure rose 0.5% in April, pushing the twelve-month comparison to 3.3%, an eight-month high. The worst part of the report was that wages continue to lose ground to inflation, as “real” inflation-adjusted hourly earnings declined 0.5% and are now down 0.3% in the past year. With the inflation picture highly uncertain in the near term, do not expect a rate change at Warsh’s first meeting as Fed Chair in June. We in the meantime will be focused on developments in the M2 money supply, which we believe is the most reliable tool for forecasting sustained inflation and which suggest that once the Iran War is resolved, inflation may drop faster than most investors expect.

Click here for a PDF version

|